Are You Prepared for an IRS Audit?

June 4, 2018

Hey Joel- Am I required to receive ongoing fiduciary training?

June 4, 2018

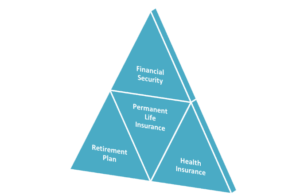

Financial security is something that every American strives for. Experts believe that the foundations of financial security are built off of three equally important pillars: a retirement plan, health insurance, and permanent life insurance. These three instruments complement one another and work together to create holistic security for individuals and their families. As an employer, offering all three of these benefits can be instrumental in attracting and retaining employees.

For decades now, the conversation around financial security at work has centered on the first two pillars of retirement and medical insurance. It is the third pillar, however, that has received relatively little attention and is equally important.

For decades now, the conversation around financial security at work has centered on the first two pillars of retirement and medical insurance. It is the third pillar, however, that has received relatively little attention and is equally important.

Many people think that a 401(k) serves the same purpose as life insurance, and for that reason, they believe you don’t need both. But the truth is, they serve very different purposes and they actually complement one another.

There is also confusion around term life insurance vs. whole life insurance. For millions of Americans, the only type they ever receive is term life insurance from an employer; however, term life insurance, by its very definition, is limited in its scope. It only provides protection for a specified “term” or period of time. How do you plan for the unexpected when the unexpected must happen during a specific time period?

Whole life insurance is the most well-known type of permanent life insurance. Just as the name suggests, it is a policy meant to provide lifelong coverage, regardless of age, affliction, or employment status.

Here are the main differences between term and whole life insurance:

|

Term Life vs. Whole Life |

|

| Provides protection for a specific, limited amount of time – ex) 20 or 30 years | Provides protection for the insured person’s entire lifetime |

| Provides no cash value. It is pure death benefit protection | Has a cash value that accumulates over the life of the policy and can be used as a benefit while the insured is living |

| Inexpensive at younger ages. Cost goes up each year. Prohibitively expensive in later years. | The higher premium cost in early years – goes towards death benefit and cash value benefit. Cost remains level for life |

The difference between term and whole life insurance can be compared to the difference between renting and owning a home. Both renting and owning provide you a place to live, and both term and whole life provide you a death benefit.

However, similar to renting, you are not building any equity while paying your term life premiums. If you own a home, each time you make a mortgage payment, you are building equity. The same is true with whole life. Each premium you pay helps you build equity in the form of the policy’s cash value, which you can use as a benefit.

Why Offer Group Whole Life?

Group whole life is a dynamic employer-sponsored solution that offers much more than a death benefit. Group whole life includes a cash accumulation component known as the policy’s cash value. The cash value is guaranteed to accumulate value over time and accumulates in a tax-deferred manner. This is a source of wealth that is available to policyholders as it accumulates. Individuals can take out loans against their policy. Additionally, some carrier group whole life policies are eligible for dividends – which can be granted in the form of cash, used to pay back loans, lower premiums, deposited to earn interest, or even used to increase your death benefit to help you keep up with inflation.

Whole life insurance is built upon three primary guarantees:

- Guaranteed premium

- Guaranteed cash value

- Guaranteed death benefit

As an employer, there are plenty of reasons to implement a group whole life policy in your benefits package:

- Bona fide employee benefit

- Suitable for SCA and Davis Bacon contractors

- Hour bank administration available

- Tax advantages

- Death benefits are generally income tax-free

- Cash values tax-deferred

- Dividends non-taxable

- Attract and retain employees

- Very few companies offer a group whole life plan

- Financially secure employees are more productive

- 65% of employees believe they need more death benefit

At the end of the day, your job is to do what is best for your business and your employees. A group whole life policy can accomplish both.

Contact your plan advisor for more information on adding group whole life insurance to your employee benefits package.

*Guarantees are based on the claims paying abilities of the issuing insurance company.

**This article was contributed to RPAG’s Retirement Times by Beneco.

{kind=link}

{kind=link}

{kind=link}