Have You Conducted a Fee Equalization/Levelization?

May 8, 2018

Evaluating Your Plan and Fees? Think More, Not Less.

May 8, 2018

As a participant in the company’s retirement plan, you are committed to saving for your future. Whether you are retiring in a few weeks or a few decades, you may need to protect your investment. A healthy way to do this is to rebalance your portfolio.

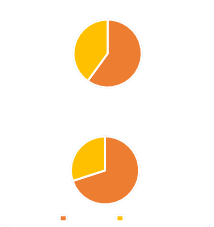

Example

Suppose you enrolled in the plan at the beginning of last year and allocated 40 percent of your portfolio to bond funds and 60 percent to equity funds. Further suppose that when you received your year-end statement, it shows that 70 percent of your assets are in equity funds and 30 percent are in bond funds. To stay within your acceptable risk level (which is what you determined before entering into the plan), you should sell enough equity funds to bring that back to 60 percent of your assets and buy enough bond funds to bring them up to 40 percent of your assets.

What is rebalancing?

Rebalancing is readjusting your portfolio back to the original asset allocation that took into account your risk tolerance and time horizon. Put another way, rebalancing forces you to adhere to your investment strategy. You rebalance by selling assets that make up too much of your portfolio and use the proceeds to buy back those that now make up too little of your portfolio. The net effect is to “sell high and buy low.” Ultimately, regular rebalancing can increase the overall return of your portfolio over time. An automatic rebalancing feature may be available through your current retirement plan provider. Visit your provider’s website for more information.Keeping in check

Experts recommend you rebalance at least once a year and no more than four times a year. Consider this a good opportunity to evaluate if your investment strategy is still in line with your original goals.If you have questions or require further assistance, please contact Tim Kunkle on Duncan Financial Group’s Financial Wellness team at tkunkle@duncangrp.com or (412) 238-7334.

Rebalancing assets can have tax consequences. If you sell assets in a taxable account you may have to pay tax on any gain resulting from the sale. Please consult your tax advisor. This material is not intended to replace the advice of a qualified attorney, tax advisor, investment professional or insurance agent.

{kind=link}

{kind=link}

{kind=link}