October Employee Of The Month- Janet Beliles

October 5, 2018

Hey Joel! – Is my 501(c)(3) organization eligible for a 401(k) plan? Are there any benefits over a 403(b) plan?

October 8, 2018

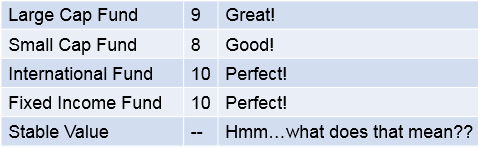

As you read your plan’s lineup, you see the following scores

:

Periodically you review your plan’s fund lineup; you place some funds on Watchlist, you replace under-performers and you continue to monitor those funds that score acceptably. But, you see a dash next to your cash fund and wonder, what should you do?

Traditional evaluation metrics can be difficult to apply to cash funds. You can look at returns, but without an appropriate benchmark or a way to directly measure the risk taken by the fund, the market value performance number can be difficult to interpret. Perhaps fees can provide the answer, but there are wrap fees, investment management fees and trustee fees, all assuming there is a stated fee to review in the first place. What is a fiduciary to do?

While cash fund due diligence can be intimidating, there are key differentiators among stable value funds that fiduciaries can review to document that a fund is a good fit for their participants. Ultimately stable value funds are not too different from other funds within a plan lineup and the strategies to evaluate them are similar. There exists an established methodology incorporated into your IPS for evaluating these standard funds. Let’s evaluate how well that framework can be applied to the stable value universe.

Traditional evaluation metrics can be difficult to apply to cash funds. You can look at returns, but without an appropriate benchmark or a way to directly measure the risk taken by the fund, the market value performance number can be difficult to interpret. Perhaps fees can provide the answer, but there are wrap fees, investment management fees and trustee fees, all assuming there is a stated fee to review in the first place. What is a fiduciary to do?

While cash fund due diligence can be intimidating, there are key differentiators among stable value funds that fiduciaries can review to document that a fund is a good fit for their participants. Ultimately stable value funds are not too different from other funds within a plan lineup and the strategies to evaluate them are similar. There exists an established methodology incorporated into your IPS for evaluating these standard funds. Let’s evaluate how well that framework can be applied to the stable value universe.

All the data points identified as key components of evaluation can be found on the RPAG stable value fund factsheets.

The first component for evaluation of the RPAG Scorecard is a fund’s style. Does the fund stick to its professed asset class? Do the same for a stable value fund’s portfolio. Is it allocating to assets and securities that are appropriate for a high-quality, short-term fixed income fund? Also evaluate the fund’s diversity of allocation. Monitoring its allocating across a variety of subsectors of fixed income (treasuries, corporate bonds, mortgage backed securities, etc.).

The next criteria is evaluation of risk and return. There are a plethora of data points for evaluating stable value fund risk and return. With regard to return, examine a fund’s crediting rate or its yield relative to the stable value universe to evaluate this fund’s performance. Similar to traditional funds, performance needs to be examined relative to the risk taken. For evaluating risk the underlying portfolio is important. Review the credit ratings of the underlying securities, verify the average duration or maturity relative to the funds’ peers, and evaluate the asset managers investing the underlying portfolio. Also review the number of wrap providers for the portfolio and their credit rating.

The final quantitative component of the RPAG Scorecard is peer group review. Once again a stable value fund’s evaluation can follow this same methodology. Evaluation of a fund’s market-to-book ratio, relative to its peers, is a key component of portfolio health and to identify potential issues early. Cash flows in and out of a fund relative to the universe give valuable insight to how quickly the portfolio can react to changing market conditions.

For qualitative components, look at the same key characteristics that are evaluated for standard funds, as well as a few unique characteristics to stable value. A long tenured and constant management team is important no matter the type of fund. Also, while there are additional fees in the stable value universe, evaluating them relative to the universe is still important. Unique to stable value is a fund’s exit provisions (is there a put, and if so how long) and the fund’s high yield policy to ensure both align with participant best interests.

Stable value funds seem unique, and they do have peculiar challenges when evaluating them, it’s still a crucial task for fiduciaries. The same process that has been established within the plan’s IPS to evaluate the core line-up, can be adapted to evaluate stable value funds in a similar manner.

The next criteria is evaluation of risk and return. There are a plethora of data points for evaluating stable value fund risk and return. With regard to return, examine a fund’s crediting rate or its yield relative to the stable value universe to evaluate this fund’s performance. Similar to traditional funds, performance needs to be examined relative to the risk taken. For evaluating risk the underlying portfolio is important. Review the credit ratings of the underlying securities, verify the average duration or maturity relative to the funds’ peers, and evaluate the asset managers investing the underlying portfolio. Also review the number of wrap providers for the portfolio and their credit rating.

The final quantitative component of the RPAG Scorecard is peer group review. Once again a stable value fund’s evaluation can follow this same methodology. Evaluation of a fund’s market-to-book ratio, relative to its peers, is a key component of portfolio health and to identify potential issues early. Cash flows in and out of a fund relative to the universe give valuable insight to how quickly the portfolio can react to changing market conditions.

For qualitative components, look at the same key characteristics that are evaluated for standard funds, as well as a few unique characteristics to stable value. A long tenured and constant management team is important no matter the type of fund. Also, while there are additional fees in the stable value universe, evaluating them relative to the universe is still important. Unique to stable value is a fund’s exit provisions (is there a put, and if so how long) and the fund’s high yield policy to ensure both align with participant best interests.

Stable value funds seem unique, and they do have peculiar challenges when evaluating them, it’s still a crucial task for fiduciaries. The same process that has been established within the plan’s IPS to evaluate the core line-up, can be adapted to evaluate stable value funds in a similar manner.

Stable Value Fund Terminology Cheat Sheet

Stable Value Funds

A cash alternative investment option within tax-qualified retirement plans. Typically invests in high-quality, short-term fixed income securities.

Wrap

An insurance contract purchased by the Stable Value fund that ensures participants are paid out at book value when they withdraw money.

Book Value

The value of the original investment increased by the stated crediting rate.

Crediting Rate

The set rate of the return the participants in the fund receives. The rate is reset at varying intervals depending on the fund.

Market Value

The value of the underlying portfolio of securities. Will often fluctuate around the book value.

Market Value Adjustment (MVA)

A liquidity restriction upon Stable Value funds that adjusts book value to market value upon an employer initiated event.

Credit Quality

The credit rating of the underlying securities within the portfolio

About the Author, Ryan Hamilton

Ryan works closely with advisors and plan sponsors on investment due diligence and in-depth analysis of manager performance and platform and provider benchmarking. Prior to joining RPAG, Ryan worked for a third-party administrator as an associate administrator managing annual compliance for defined contribution and defined benefit plans. He earned a Bachelor of Arts degree from UCLA and is a CFA Level III Candidate.

Ryan works closely with advisors and plan sponsors on investment due diligence and in-depth analysis of manager performance and platform and provider benchmarking. Prior to joining RPAG, Ryan worked for a third-party administrator as an associate administrator managing annual compliance for defined contribution and defined benefit plans. He earned a Bachelor of Arts degree from UCLA and is a CFA Level III Candidate.

{kind=link}

{kind=link}

{kind=link}